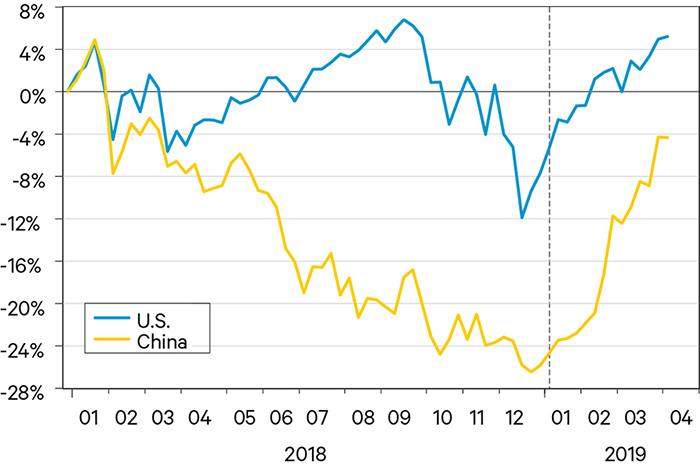

The world breathed a sigh of relief when the U.S. announced that there would be no additional tariffs imposed on Chinese imports on the March 31, 2019 deadline. The explanation was that the trade negotiations between the U.S. and China were making progress. A full-blown trade war was avoided, for the moment. Although equity markets react to many different news items affecting company profits, it is not a coincidence that the Shanghai Composite index rebounded and almost recovered most of its loss in 2018 (Figure 1, red line), and the U.S. S&P 500 index (Figure 1, blue line) turned around at approximately the same time. But will an agreement take place? There are difficult issues still to be resolved. Nevertheless, there is some indication that movement towards a limited agreement is occurring.

The information being reported in the press points to concessions on the part of both China and the U.S. that might be part of a modest trade deal. However, one should view this information skeptically as the release of it might well be a negotiating tactic. In the end, some may not be included in an agreement. Both Xinhua Press and Trump Administration officials have signaled that the following chapters are being negotiated:

Some of the items mentioned above are straightforward, less controversial, and likely have been agreed to. For example, a recent announcement by China that it would ban all variants of the opioid fentanyl, a U.S. request, is an easy concession to make. The purchase of more U.S. agricultural produce (at the expense of other countries’ farmers) is also relatively easy. These are signals of goodwill that China is likely hoping will bring the negotiations to a mutually beneficial close.

On the other hand, as we have discussed in previous reports, controversial demands on the part of the Trump Administration, which go to the heart of Chinese domestic economic policy, will be difficult if not impossible to resolve including:

In a commentary in Xinhua, as reported by the South China Morning Post, Chinese officials view the remaining issues as “tough nuts to crack.” We agree, but expect both countries to find some common ground in order to close a trade deal in the near term, and agree to continue talks on other issues in the future.

But, keep in mind that a new trade agreement does not mean there will be no tensions nor disputes between these, the two largest economies in the world, in the coming years. As we mentioned in previous reports, the world is in a new era of strategic competition between the U.S. and China, particularly in the fields of science and technology. For example, last month the U.S. Chairman of the Joint Chiefs of Staff told a U.S. Senate panel that Google’s work in China has been directly benefiting China’s military. In response, Google said it had dropped some ideas it had been pursing with the Chinese government. We expect more of this state scrutiny and regulation with respect to technologically sophisticated products and services in the future.

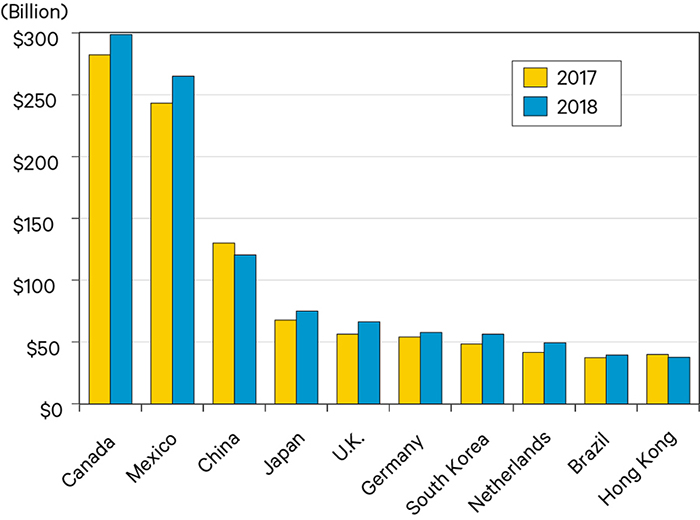

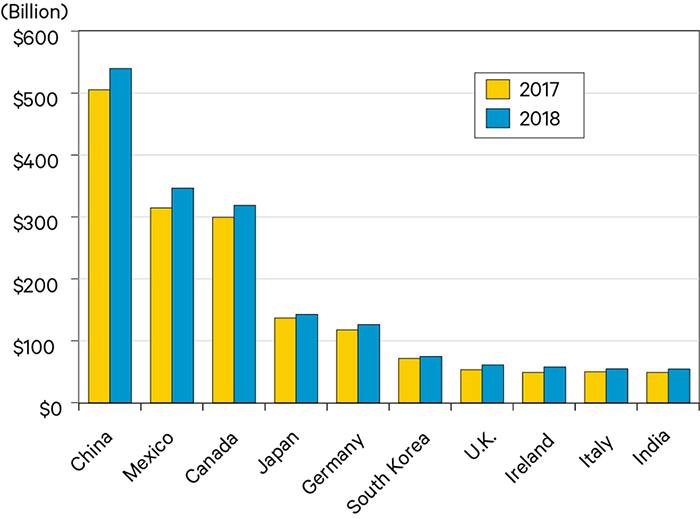

Figure 2 displays the top ten trading countries for U.S. goods exports in 2017 (yellow bar) and 2018 (blue bar). All of the trading partners have seen U.S. exports increase with the exception of China and Hong Kong. The obvious reasons are China’s retaliation against the U.S. tariffs, and the slowing growth of China’s economy. The top three countries for U.S. exports in 2017, Canada, Mexico, and China, are the top three in 2018. Figure 3 displays the top ten trading countries for U.S. goods imports in 2017 and 2018. U.S. imports from all of its top trading partners increased last year. This includes China despite tariffs imposed on $250 Billion of Chinese imports. At least for now, the tariffs represent a tax on American consumers and not on Chinese producers.

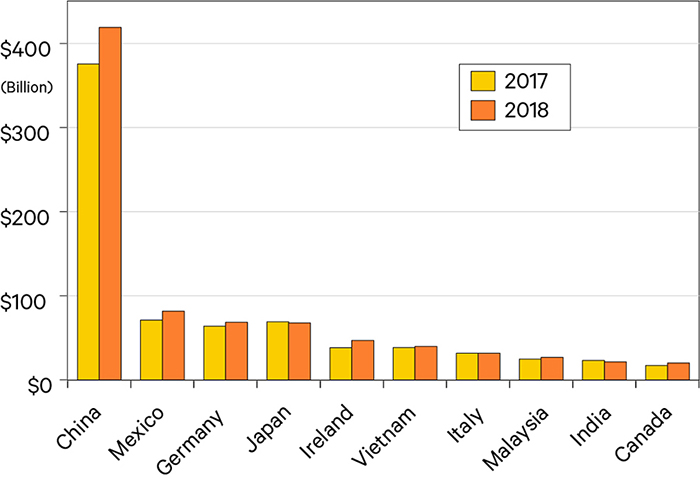

Figure 4 shows the top ten countries with trade deficits with the U.S. by the size of the deficit. China has the largest deficit accounting for about half of the total deficit. The China trade deficit increased from $376 billion in 2017 to $419 billion in 2018. While this is not surprising given that job growth and consumption are growing in the U.S., and given that the U.S. government’s fiscal deficit is expanding rapidly and needs financing, it is in the opposite direction from the goal stated by the Trump Administration.

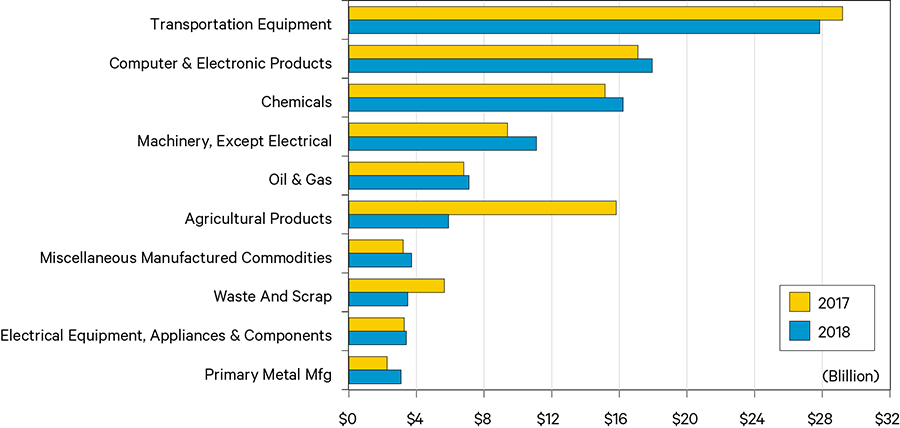

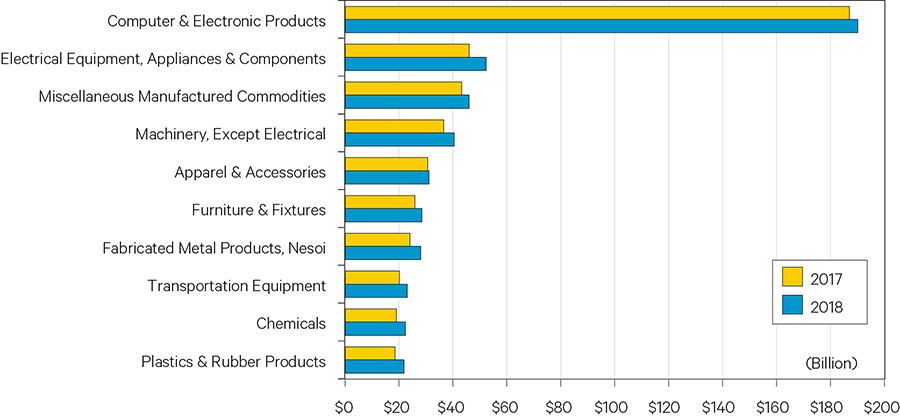

Figure 5 displays the top 10 U.S. export goods to China in 2017 (yellow bar) and 2018 (blue bar). Only three sectors experienced a decline in exports value in 2018: (1) transportation equipment, (2) agricultural products, and (3) waste and scrap. In particular for agricultural products, its decline from $16 billion in 2017 to $6 billion in 2018 was staggering. This is a direct result of Beijing’s tariff and purchasing decisions, and as it happens it fell on rural counties in the U.S. where the President’s support is the highest. By value (Figure 6) imports in each of the leading import sectors increased over the last year.

The economic relationship between the U.S. and China may bifurcate into a two-tier trading relationship in the future. One tier, some consumer goods, services, some investment, and tourism, would resume in a relatively free trade environment were new trade agreement to be reached. The other tier, goods and services involving advanced technology, information, communication, and national security, will be governed by strategic competition parameters rather than free trade. The question of this update to the annual Cathay Bank / UCLA Anderson Forecast U.S. - Economic Report remains open. Will there be an agreement? We now have some solid indications that the modest agreement we have been predicting in this series is coming to realization.

Cathay Bank has established a sponsorship relationship with UCLA Anderson Forecast to produce a U.S.-China Economic Report. In this report, UCLA Anderson Forecast will talk about their view of economic analysis and perspective on the current and future outlook relating to the two largest economies in the world – the United States and China.

UCLA Anderson Forecast has been the leading independent economic forecast of both the U.S. and California economies for over 65 years. The annual report and quarterly columns written by UCLA Anderson Forecast will focus on current topics affecting investment flows and associated economic events between China and the United States.

This report includes forecasts, projections and other predictive statements that represent UCLA Anderson Forecast’s economic analysis and perspective on the current state and future outlook of the economies of The United States and China in light of currently available information. These forecasts are based on industry trends and other factors, and they involve risks, variables and uncertainties. This information is given in summary form and does not purport to be complete. Information in this report should not be considered as advice or a recommendation to you or your business in relation to taking a particular course of action and does not take into account your particular business objectives, financial situation or needs.

Readers are cautioned not to place undue reliance on the forward-looking statements in this report. UCLA Anderson Forecast does not undertake any obligation to publicly release the result of any revisions to these forward-looking statements to reflect the occurrence of unanticipated events or circumstances after the date of this report. While due care has been used in the preparation of forecast information, actual results may vary in a materially positive or negative manner. Forecasts and hypothetical examples are subject to uncertainty and contingencies outside UCLA Anderson Forecast’s control.

Jerry Nickelsburg joined the UCLA’s Anderson School of Management and The Anderson Forecast in 2006. Since 2017 he has been the Director of The Anderson Forecast. He teaches economics in the MBA program with a focus on Business Forecasting and on Asian economies. He has a Ph.D. in economics from the University of Minnesota and studied at The Virginia Military Institute and George Washington University. He is widely published and cited on issues related to economics and public policy.

William Yu joined the UCLA Anderson Forecast in 2011 as an economist. At Forecast he focuses on the economic modeling, forecasting and Los Angeles economy. He also conducts research and forecast on China’s economy, and its relationship with the US economy. His research interests include a wide range of economic and financial issues, such as time series econometrics, data analytics, stock, bond, real estate, and commodity price dynamics, human capital, and innovation.