According to the 2018 WalletHub survey, only 41% of people check their credit reports more than once a year, though 84% say they know they should be checking more often.

The reason for the low percentage shows a lack of understanding of credit reports and scores: 27% said they do not have time to check their reports more often; 35% said they did not want to be charged for reading it, though free credit reports are available; and 14% said they were afraid to see what would be in the report.

Credit reports are typically generated for lenders and financial professionals to review to determine loan application decisions. These reports are not designed for the average person to read. However, as more Americans become financially sound and want to take charge of their own credit destiny, they are pulling their credit reports for their own review.

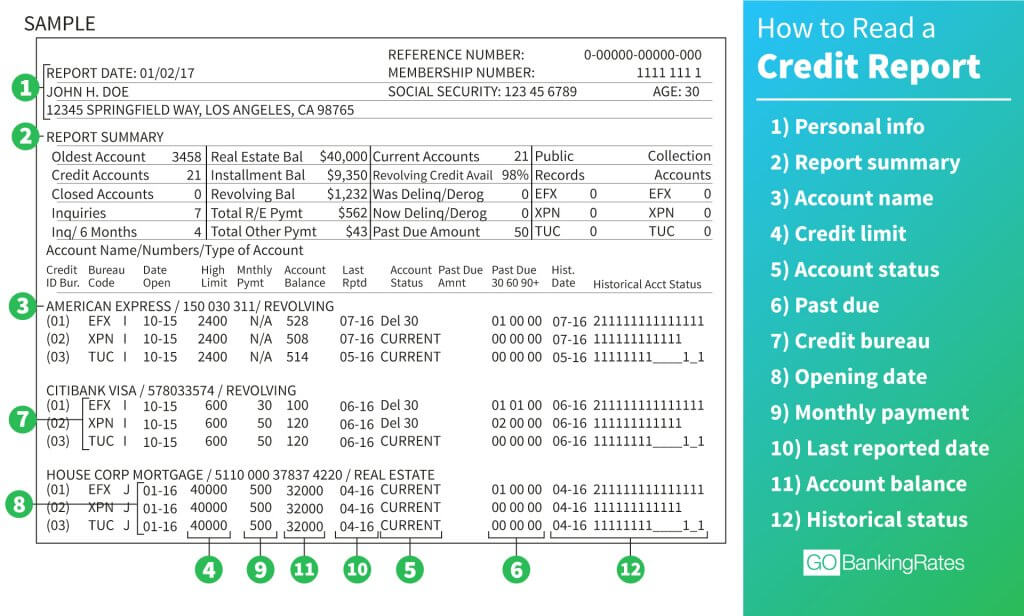

In the sample credit report below, you can see how complex a credit report is to read.

Nghi Trang, financial well-being coach for Operation HOPE Inc., provides some insights and breaks down the components of a credit report into four sections.

Your credit report can be broken down into four main categories:

This section will list your name and aliases, Social Security number, date of birth, employment data, and current and previous addresses. You should review this section to make sure your information is correct. Be extra cautious if your name is very common, like John Smith or Maria Garcia. Information can easily be mixed up in situations like these.

If you need to make any corrections in this section, you will need to write a letter to each of the three credit bureaus (Equifax, TransUnion, and Experian) to state the error and what the correct information should be. The agencies will require proof of identity, so include a copy of your driver’s license and Social Security card with your letter.

This section will list any bankruptcies, liens, or judgments you have had. Most people will find this section empty because these are not common situations. If you see anything in this section that does not belong to you, immediately contact the three credit bureaus to ask them to remove these items from your credit report.

Because of the codes used in this section, this is the most confusing part of your credit report. This section lists the status of the account (current, open, closed, collections, or charged off), responsibility (joint or individual), account balance, most recent payment, past-due information (if applicable), and credit limit. There is a lot of information in this section, so codes are used to make it more compact; however, when it comes to reading it, the average person will be lost.

In the simplest terms, you want to see an "OK" on your TransUnion or Experian credit reports or an asterisk on your Equifax report. These indicators show that there is no problem with your payment history.

This section will show all the hard inquiries that have been run on your credit report. It lists the dates and names of the financial institutions that pulled your credit report for a loan application.

Too many hard inquiries will lower your credit score because it establishes a trend that you are in need of borrowing. When you pull your own credit report for review, it is a soft credit pull and will not affect your credit score.

If you still need help with your credit report, you are not alone. There are resources available to help you navigate this process.

Operation HOPE is a nonprofit organization that provides free financial literacy workshops and one-on-one credit counseling to the community.

An Operation HOPE financial well-being coach will pull your credit report and review each section line by line. The coach will help you draft dispute letters for any incorrect personal information or show you how to negotiate deals to resolve collections accounts. The coach will provide step-by-step identity theft resolutions. Operation HOPE provides these services free of charge.

If you have pulled your credit report and feel overwhelmed, if you were declined and cannot figure out why, or if you have not checked your credit report in a long time, reach out to an Operation HOPE financial well-being coach for help.

To find Operation HOPE locations throughout the United States, visit https://operationhope.org/our-locations/. In Orange County, California, visit the Operation HOPE in the same building as our Westminster branch:

HOPE Inside Westminster Cathay Bank

9121 Bolsa Avenue Suite 202

Westminster, CA 92683

657-200-5073

Operation HOPE is an independent third party unrelated to Cathay Bank and Cathay General Bancorp.

This article does not constitute legal, accounting or other professional advice. Although the information contained herein is intended to be accurate, Cathay Bank does not assume liability for loss or damage due to reliance on such information.